- Home

- Government

- Board of County Commissioners

- Property Assessment Appeal

- Understanding the Property Tax Process

Understanding the Property Tax Process

The County Property Assessment and Appeal Process

What’s My Property Worth?

Let’s begin by understanding where property assessment occurs in the property tax process.

NOTE - Please be advised that this document is for general informational purposes only, is not legal advice, you should consult with your legal counsel regarding your specific rights or responsibilities.

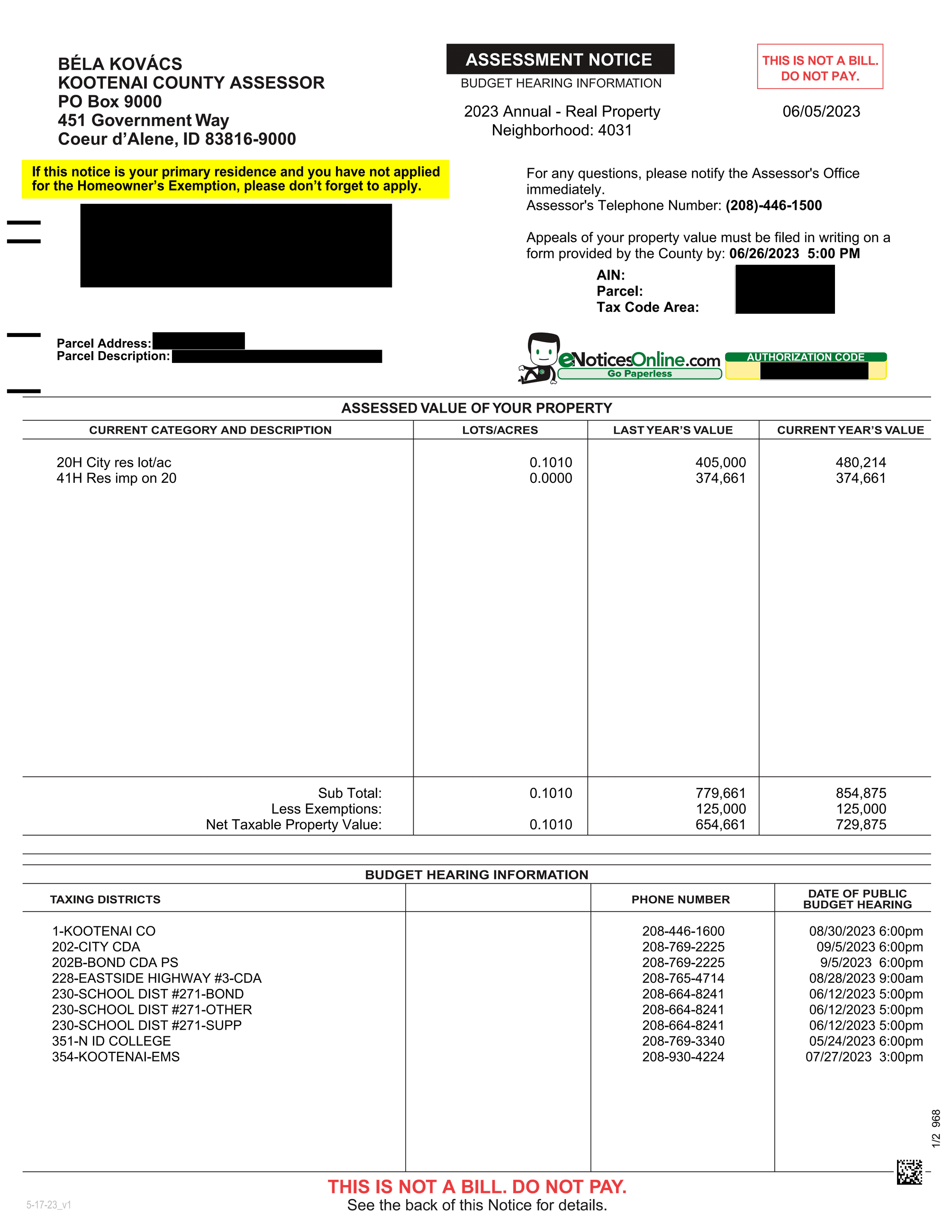

First – The County Assessor finds the market valuation for every property throughout the county for assessment purposes. Assessment notices are mailed out at the end of May.

Second – Taxing districts establish their budgets – There are about 45 taxing districts and several special assessments in Kootenai County. A typical property will lie within the boundaries of 4-10 of these taxing districts. Each of those taxing districts are made up of elected board members. These boards will develop their budget for the upcoming fiscal year. Each board will predict anticipated revenues verses expenses and the remaining balance becomes the requested property tax levy (budget $ needed that must come from property taxes) for each taxing district. This budget formation activity typically occurs during the months of April through August. All budget meetings are open to the public.

Third – The County Auditor calculates a levy rate – This is accomplished by dividing the total tax levy by the total valuation of all properties within the boundaries of each of the 44 taxing districts. This decimal property tax levy rate value (example .002020179) is then multiplied against the assessed valuation of your property after exemptions. This produces that property’s fair share of the monies needed by each taxing district. If there are separate voter approved levies or bonds they are also calculated. This calculation activity occurs in the months of October and November and is computed for each of the over 90,000 properties in Kootenai County.

Fourth – On behalf of all the taxing districts the County Treasurer creates each property tax bill – The Property Tax bills are mailed out at the end of November.

Fifth – Payments are received – The Treasurer and Auditor distribute the tax levy dollars to each respective taxing district that they are due.

You received your assessment notice, now what?

Idaho’s property tax system depends on all properties being assessed accurately. Annual property assessment reviews are how each property owner can be assured each property is being assessed equally to reflect market conditions in your neighborhood. A property worth $1 million should be assessed at $1 million. A property worth $100,000 should be assessed at $100,000. In this manner, property owners can be assured that everyone is paying their fair share of the tax burden. No more, no less. Your property assessment value is a reflection of what your property would likely sell for if listed for sale as of January 1st of the current year.

Step #1

Review the statement for accuracy

- Is the property size correct? (i.e. 5.0 acres)

- Do the valuations of the property and improvements to the property seem reasonable based on market sales in your neighborhood?

- Did you make any improvements to your property in the last few years that may have caused the property value to increase?

- Is there something not typical about your home compared to other homes in the neighborhood that would make its market value significantly less than others in your neighborhood?

- Do you have other improvements (shop, landscaping, paving, concrete, etc) that might increase your value above others?

- If you decided to list your property for sale, and based upon sales in your neighborhood, would you list it for more or less than the value shown on your assessment notice?

- IF you qualify for an exemption, is it reflected in your assessment notice? (Some exemptions must be applied for each year and all exemptions require an application).

Step #2

A few points about the property assessment

- The Assessor is required to follow Idaho law regarding the assessment on your property and while a mistake can sometimes occur, the Assessor’s team is generally very accurate and follows the requirements of the law.

- The Assessor must appraise your property and all other properties in Kootenai County at fair market value.

- There are over 92,000 properties in Kootenai County that are assessed by the Assessor’s Office each year.

- Your assessment notice reflects the market value of your property as of January 1st of the year you receive your assessment notice.

- By law, the value established by the Assessor must be within 90%-110% of fair market value (based on property sales information).

- The Assessor must make, or attempt to make, a physical inspection once in a 5-year cycle. It is not uncommon that the Assessor finds significant improvements made to properties based on these physical inspection visits. If you property jumped significantly this year, it may be related to: (a) the physical inspection revealed improvements not known by the Assessor before, or; (b) your neighborhood is a ‘hot market” resulting in higher market sales data for your neighborhood.

- The Kootenai County assessment process and assessed valuations are reviewed by the State Tax Commission to ensure they fall within the 90-110% range.

(a) “Market value" means the amount of United States dollars or equivalent for which, in all probability, a property would exchange hands between a willing seller, under no compulsion to sell, and an informed, capable buyer, with a reasonable time allowed to consummate the sale, substantiated by a reasonable down or full cash payment

Step #3

You believe something is wrong with your assessment

- The first place to go with questions about your assessed valuation is to the Assessor’s Office.

Contact Info: Assessor’s Office

208-446-1500

M-F 9:00am – 5:00pm

- As the property owner, you may have some information that the Assessor does not possess. For example, you may know some particulars about your property that makes its valuation worth less than the value the Assessor established.

- Begin by writing down details about your property/home that you feel make your home/property worth less than what homes in your neighborhood sold for in the prior year.

- If you have direct knowledge about prior home sales that occurred in your neighborhood that are not representative of your home or others in your neighborhood, (perhaps several of those homes had much higher quality of construction) write those differences out and bring them with you when you come in to talk to the Assessor.

- To support your case for a lower valuation request, the Assessor may agree to meet with you on your property to talk through the home and other structures.

Step #4

No luck after visiting the Assessor? Appeal to the Board of Equalization (BOE)

The Assessor and his team are highly qualified. It is rare that they over assess a property. If you did not provide very specific information that persuaded them to lower your valuation, your changes of convincing others may not be successful. Please understand that the steps that follow could result in: (1) no change in value, (2) the value being lowered, or (3) the value being raised higher than the value calculated by the Assessor. However, if you believe you would like to appeal the valuation you can proceed with your appeal to the Board of Equalization (BOE). If you still do not get the results you desire, you may then appeal to the Idaho State Board of Tax Appeals. If that is unsuccessful, you could pursue legal relief in district court.

BOE APPEAL: You can appeal the assessment to the Board of Equalization (BOE) which is the Kootenai County Board of Commissioners. The 4th Monday in June is the deadline to apply for appeal.

- The BOE is a ‘hearing’ and operated very much like a court and serves in a quasi-judicial capacity.

- Please realize that the Assessor will be in the appeal hearing arguing to keep the value where it is and the Assessor will have supporting evidence for their valuation determination.

- This will be a legal proceeding, anyone testifying will be sworn in under oath. You may hire an attorney to represent you. If you do, you will need to provide an “Affidavit of Property Owner”. Attorneys representing owners must be licensed to practice law in Idaho.

- Please be aware that these hearings are public hearings and are a matter of public record. Citizens may sit in and/or request records of your testimony.

- If you plan to appear in person, you must provide at least 5 copies of all evidence you would like to be considered.

- The BOE can only lower your valuation on solid credible evidence that your property value should be reduced. Your personal opinion of value, by itself and without supporting evidence of market value, is unlikely to present a compelling case such that your property value will be altered by the BOE. Making changes to any single property can create inequities to other properties. To keep the assessment system and process sound and fair to everyone, the BOE cannot make arbitrary adjustments to individual property valuations.

- Please consider that you will have approximately 10 minutes to make a compelling case that your assessment was incorrect. The Assessor’s appraisers will also present their case and you both will be allowed to rebut the other. The BOE board may ask you questions and then they will deliberate to reach a decision.

- Even if the BOE were to decide to lower the value of your property, the Assessor may appeal the BOE decision to the Idaho State Board of Tax Appeals.

IDAHO STATE TAX BOARD: If you do not like the BOE ruling, you can appeal the assessment valuation to the “Idaho State Board of Tax Appeals” https://bta.idaho.gov/. You can find the form <here>.

LAWSUIT: Filing a lawsuit is the final option available to you.

Idaho Code §63-502

The function of the board of equalization shall be confined strictly to assuring that the market value for assessment purposes of property has been found by the assessor, and to the functions provided for in chapter 6, title 63, Idaho Code, relating to exemptions from taxation. It is hereby made the duty of the board of equalization to enforce and compel a proper classification and assessment of all property required under the provisions of this title to be entered on the property rolls, and in so doing, the board of equalization shall examine the rolls and shall raise or cause to be raised, or lower or cause to be lowered, the assessment of any property which in the judgment of the board has not been properly assessed. The board of equalization must examine and act upon all complaints filed with the board in regard to the assessed value of any property entered on the property rolls and must correct any assessment improperly made. The taxpayer shall have the burden of proof in seeking affirmative relief to establish that the determination of the assessor is erroneous, including any determination of assessed value. A preponderance of the evidence shall suffice to sustain the burden of proof.

[63-502 added 1996, ch. 98, sec. 6, p. 344; am. 2003, ch. 266, sec. 2, p. 704.]